Previously, CYL’s clean balance sheet made it an attractive takeover target, according to a corporate observer. “The company’s clean balance sheet attracted a lot of suitors in the past. However, the founder wants to pass the company to the next generation,” the observer says of CYL, which has no debt and is currently sitting on RM7.29 million cash (as at Jan 31).

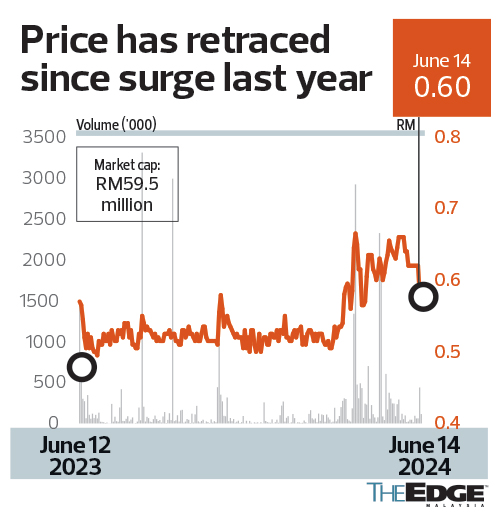

In January last year, CYL’s share price surged as high as RM1.18, even though it had slipped into the red. Market observers attributed the interest to a potential buyout, although Chen denies there was such an approach.

“I’m not aware. As of now, the company is working on new opportunities in property development. We are also looking for ways to expand the sales of our core business,” he says.

“So far, we don’t see any alternative in the plastic packaging sector. As such, the core business is still viable and we expect more demand moving forward.”

CYL’s share price had since retraced to 60 sen last Friday, giving the company a market capitalisation of RM59.5 million. The shares are highly illiquid as 57% of the company is held by the Chen family, with the free float at 21%. Year to date, the average daily trading volume stands at 204,000 shares.